As the UK mortgage market moves through the final quarter of 2025, our latest Mortgage Market Briefing highlights a market that remains resilient and forward-looking.

Mortgage applications are up more than 7% year-on-year, signalling renewed borrower confidence despite wider economic uncertainty. Average mortgage rates have fallen by 21 basis points over the past year to 4.43%, saving borrowers around £300 annually.

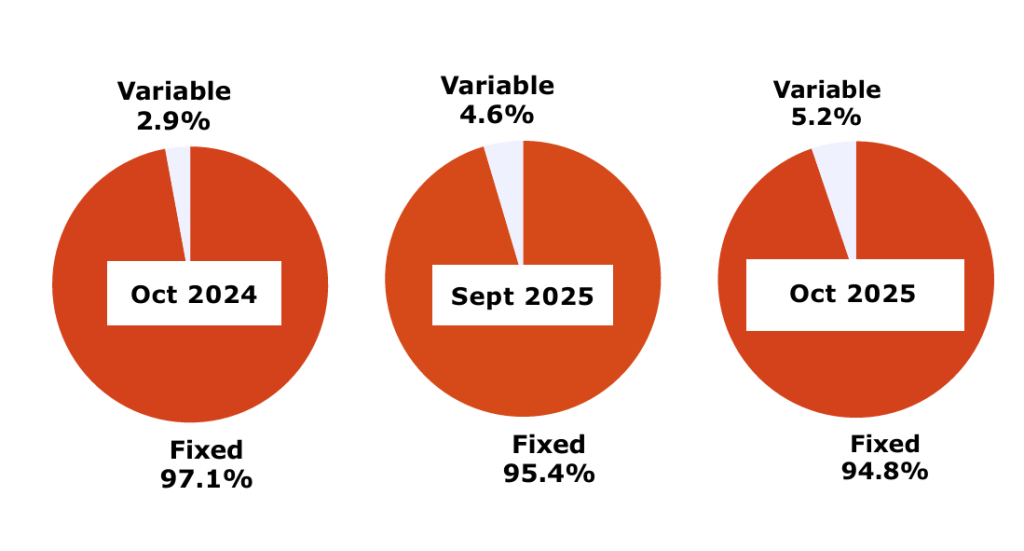

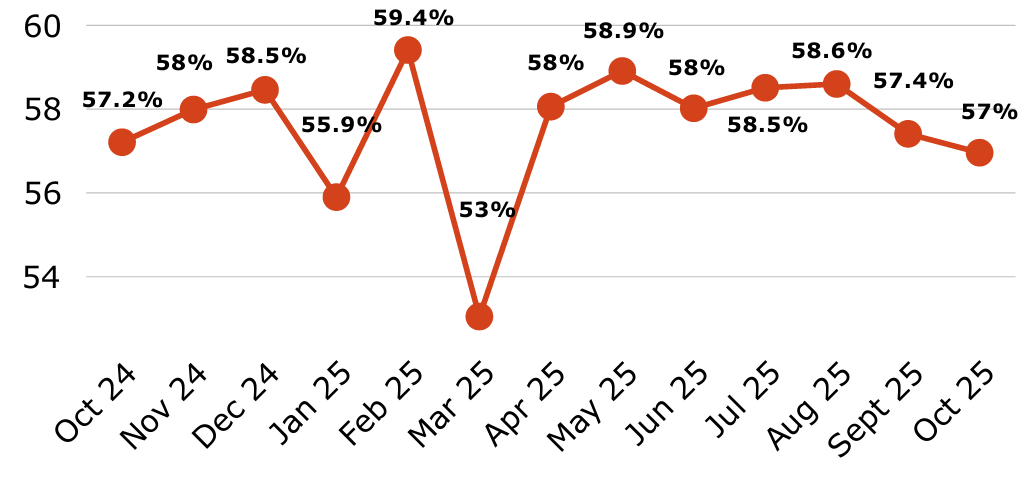

Fixed-rate lending continues to dominate at over 95% of all new loans, yet shorter-term and variable-rate products are attracting growing interest as rate cuts edge closer. Remortgaging remains the primary driver of activity, accounting for nearly two-thirds of lending, but purchase demand is also holding firm as affordability conditions gradually improve.

Commenting on October’s findings, Rob Clifford, Stonebridge Chief Executive said:

“The fact that mortgage applications are up more than 7% year-on-year shows the market is still moving forward despite wider economic uncertainty and speculation around the Autumn Budget.

“One of the key reasons is that lenders continue to compete aggressively. Many of the major high street names have reduced rates in recent weeks, meaning the average borrower is now saving around £300 a year compared to 12 months ago. That may seem a small saving, but it all counts at a time where many people are still struggling with the rising cost of living.

“If we see another rate cut before the end of the year, as expected, that could provide even more momentum as we head into 2026. Combined with the large volume of fixed-rate loans due to mature this year and next, we expect activity to strengthen further over the coming 12 months.”

Fixed vs. Variable

“Fixed-rate mortgages remain the clear product of choice for borrowers, but in recent months we’ve seen a small yet notable rise in the number opting for variable rates.”

Fixed deals offer the security of predictable repayments, which is particularly attractive at a time of uncertainty. However, a growing group of borrowers appear willing to accept the risk of fluctuating payments, betting that rates will fall further as widely forecast.

One reason fixed rates continue to dominate is the Bank of England’s cautious approach to cutting interest rates.

However, if the Bank begins signalling that it is prepared to go further and faster than markets currently expect, variable rate products could stage a comeback.”

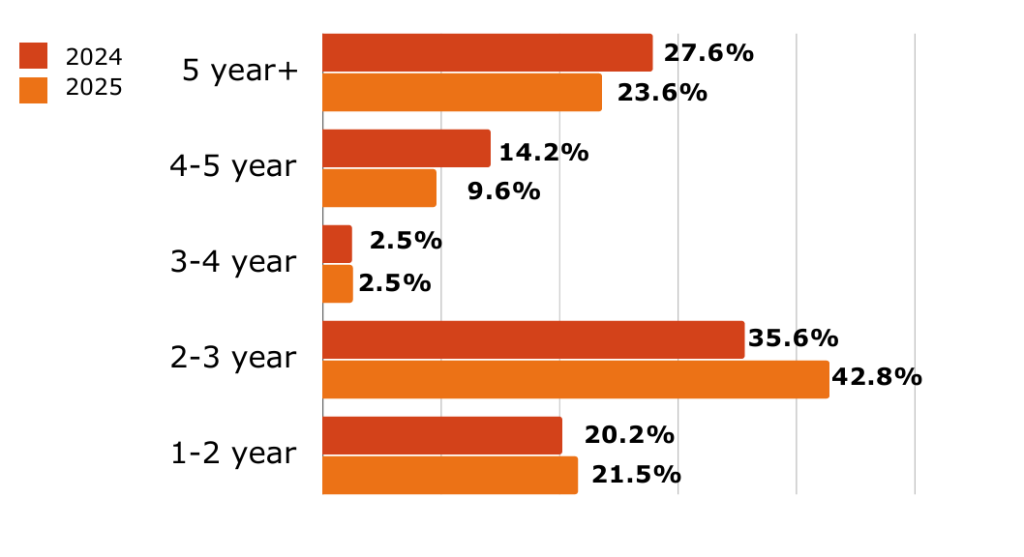

Product Length Preference

“Although interest rates have fallen considerably over the past year, the Bank of England has maintained a cautious tone, which has discouraged many borrowers from opting for variable rate deals.

“Although interest rates have fallen considerably over the past year, the Bank of England has maintained a cautious tone, which has discouraged many borrowers from opting for variable rate deals.

What we have seen instead is a surge in demand for short term fixed rates. These products offer the best of both worlds – protection from immediate rate volatility without being locked in for the long term. Many borrowers see this as a sensible middle ground, allowing them to benefit from potential future rate reductions while retaining a degree of certainty.

But since August’s unexpectedly low inflation reading, sentiment has shifted. Markets are now pricing in another rate cut before the end of the year, rather than waiting until spring. If that materialises, we could see more borrowers choosing to lock into longer-term deals to secure an attractive rate in case the outlook shifts again.”

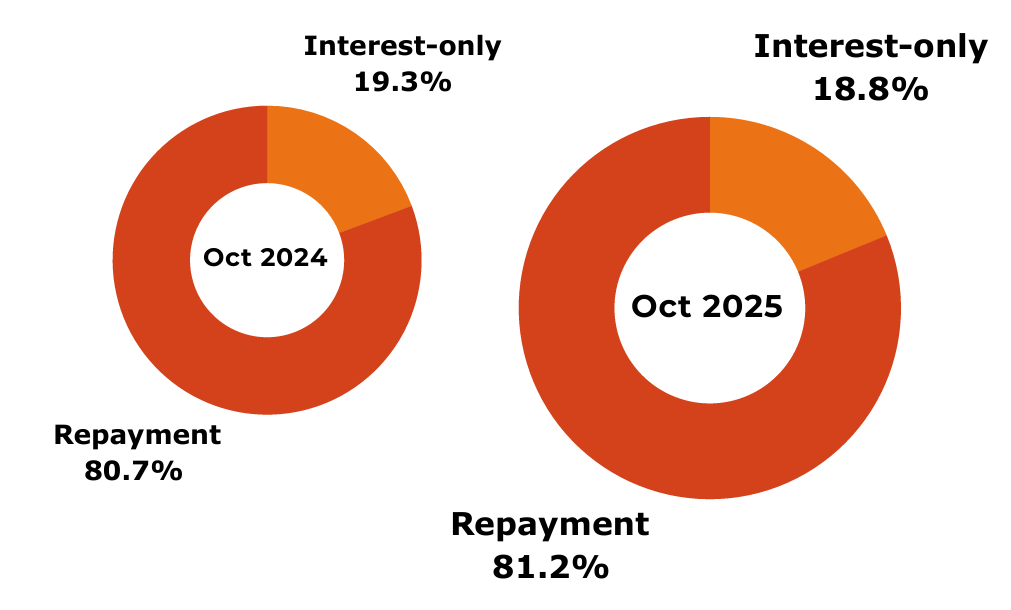

Repayment vs Interest-only

“The split between repayment and interest-only loans has remained largely static over the past year, with the latter accounting for just under a fifth of all mortgages. Typically, these options are reserved for those with higher incomes, sizeable bonuses or solid repayment plans in place, such as the sale of a second property.

However, if the Financial Conduct Authority (FCA) makes it easier to apply for an interest-only loan as part of its review of mortgage rules, we could see that tick up over time. The regulator is considering whether sale of property should be considered a suitable repayment vehicle, which would allow many more borrowers to qualify for these types of loans. That could be transformative for their popularity.”

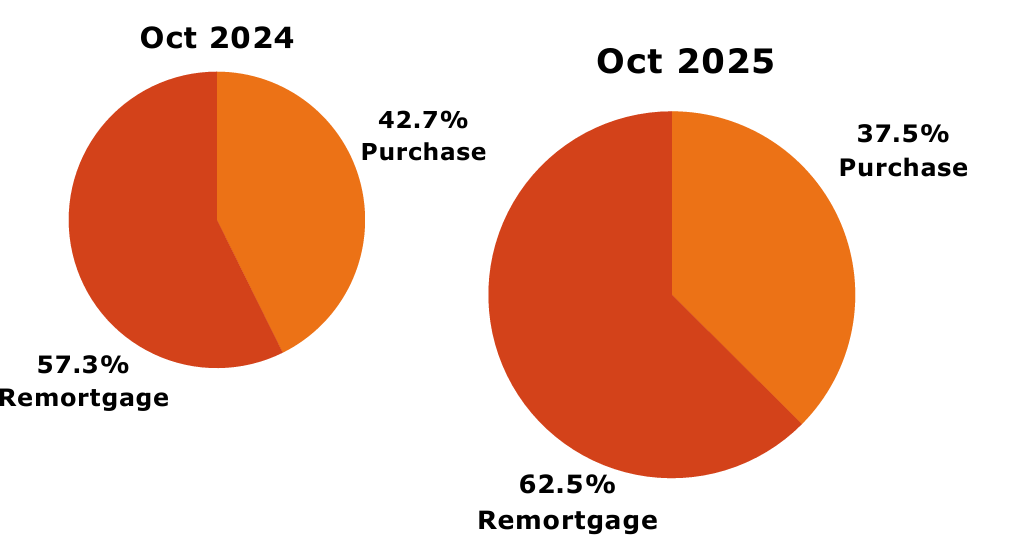

Purchase-Remortgage Split

“This has been a strong year for refinancing, with around 1.6 million fixed-rate loans up for renewal this year. It’s therefore no surprise that remortgages and product transfers made up nearly two-thirds of activity in October.

At first glance, the data might suggest that the purchase market is subdued, but that’s not the case. Purchase lending has exceeded last year’s levels in almost every month so far this year. It’s simply the sheer volume of loans maturing in 2025 that has tilted the market towards refinancing.

Looking ahead, if the Bank of England’s Monetary Policy Committee cuts rates another two or three times, as some expect, that should help restore balance. Lower rates tend to boost confidence among both movers and first-time buyers, which could boost purchase activity in the market.”

Average loan-to-value

“Average loan-to-values have declined for the second consecutive month in October, reaching their lowest level since March, although the month-on-month changes remain marginal.

This is likely a result of flat house prices combined with borrowers choosing to put down larger deposits to secure lower rates. While mortgage rates have eased over the past year, they are still high by historical standards, so it’s logical for households to reduce their repayments if they are in a position to.

Conditions for first-time buyers, who typically have smaller deposits, are gradually improving. If that continues, we could see average LTVs begin to edge higher again. But that shift will take time, and for now the trend reflects a cautious mindset among borrowers.”

Stonebridge is one of the largest independent networks in the UK that currently authorises and supervises more than 1,300 advisers across the UK.

Independent industry research has recently shown that more AR firms have chosen to join Stonebridge in 2025 than any other mortgage and protection network.

If you’re looking for a network to support you and your business with a market-leading level of support and technology, contact us here to discuss how our proposition can help.